Before signing a business broker agreement, every seller should understand the five contract areas that most commonly shift risk from the broker onto the seller: retainers, minimum fees, and termination penalties; success fee triggers; tail periods; exclusivity and automatic renewal; and dual agency. Brokerage contracts are not standardized — they vary significantly from firm to firm, and the International Business Brokers Association (IBBA) does not mandate a uniform agreement. Most business owners will sign a brokerage contract only once or twice in their lifetime, while brokers negotiate these agreements every week. That asymmetry means sellers need to know what is standard, what is reasonable, and where contract language can quietly turn against them.

This article outlines common brokerage contract clauses, their legitimate purposes, and when they cross the line into predatory territory. Whether you are actively selling your business or interviewing brokers for the first time, use this as a reference before you sign.

In This Article

- What Is a Business Broker Agreement?

- 1. Retainers, Minimum Fees, and Termination Penalties

- 2. Success Fee Triggers

- 3. Tail Periods

- 4. Exclusivity and Automatic Renewal

- 5. Dual Agency

- Quick Reference: Market Standard vs. Red Flag

- A Market-Standard Contract Checklist

- Frequently Asked Questions

What Is a Business Broker Agreement?

A business broker agreement (also called a listing agreement or engagement letter) is the contract between a business owner and a broker that governs the terms of the sale engagement. It defines the broker's responsibilities, the commission structure, the duration of the relationship, and the conditions under which the broker earns a fee.

For Main Street businesses — typically those under $5 million in revenue — the standard commission structure is a success fee of 8–15% of the sale price, paid by the seller at closing. According to the IBBA Market Pulse Survey, the majority of Main Street transactions use a success-fee model, meaning the broker earns most of their pay when the deal closes. This structure aligns the broker's incentives with the seller's: the broker gets paid when the seller does.

The five clauses below are where that alignment can break down.

1. Retainers, Minimum Fees, and Termination Penalties

Broker contracts often include upfront or fixed-fee components alongside the success fee. These come in two legitimate forms — retainers and minimum fees — but problems arise when either is structured as a disguised termination penalty.

Retainers

A retainer is an upfront fee paid at the start of the engagement to cover the broker's preparation costs: valuation work, marketing materials, CIM preparation, data room setup, and initial buyer outreach. Retainers can be good practice. They demonstrate the seller's commitment to the process and give the broker resources to invest in quality work from day one. A retainer is often credited against the final success fee, so it does not increase the seller's total cost — it simply shifts a portion of the payment forward.

What's market: A modest upfront retainer — perhaps up to $10,000 depending on the size and complexity of the business — credited against the success fee at closing. The retainer should reflect the broker's actual preparation costs, not a percentage of the expected sale price.

Minimum fees

A minimum fee (or commission floor) ensures the broker earns at least a certain dollar amount if the deal closes — for example, "10% of the sale price or $30,000, whichever is greater." Minimum fees are also standard and reasonable. The fixed costs of marketing and managing a sale are similar regardless of deal size, so a commission floor protects the broker from doing months of work on a smaller transaction for a disproportionately small payout.

What's market: A minimum commission floor that is proportionate to the scale of the business and payable only upon a successful closing. What is reasonable for a $5 million business with multiple locations and financial complexity is not reasonable for a $500,000 owner-operated business.

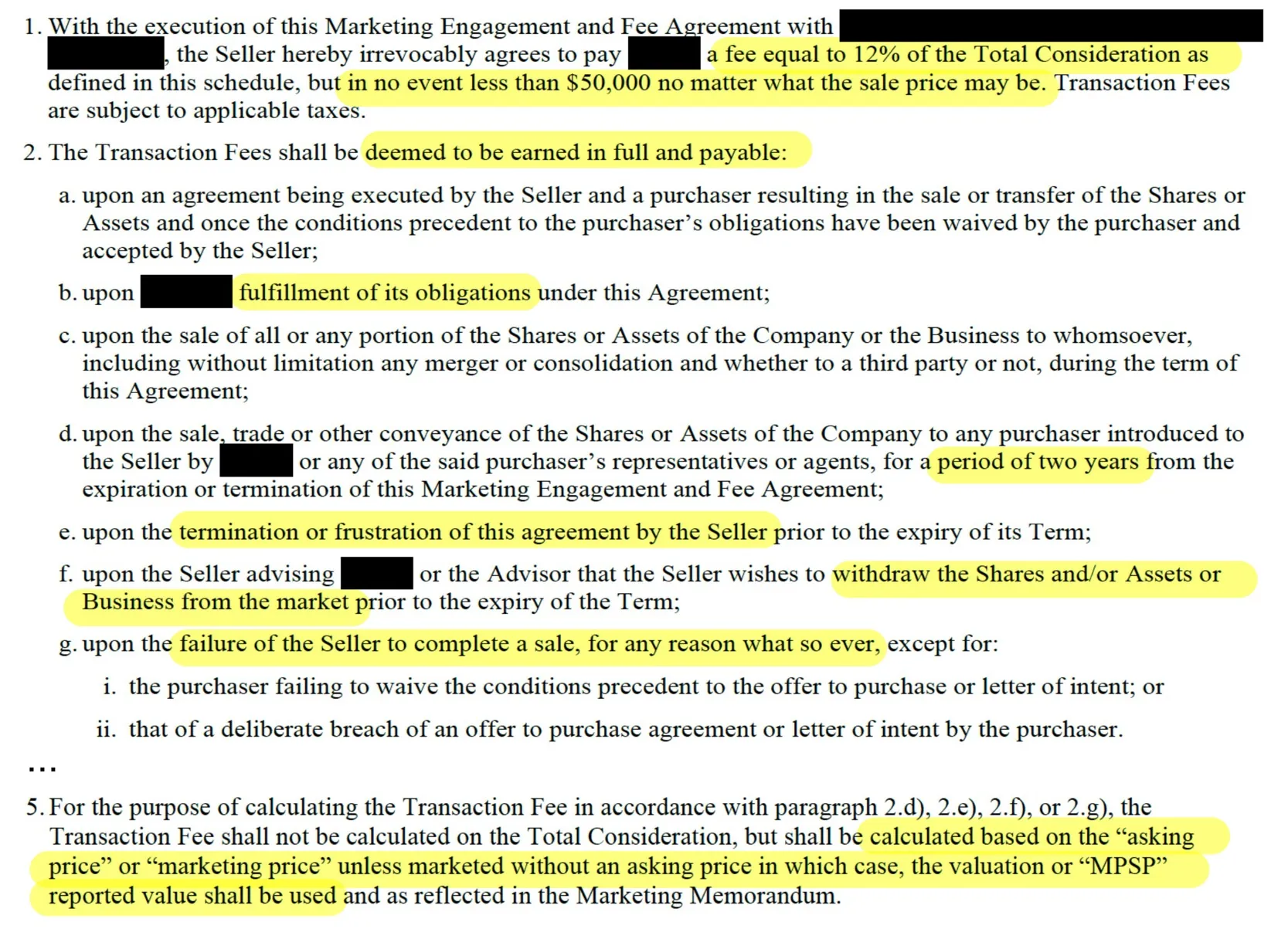

Termination penalties — where fees become red flags

Neither retainers nor minimum fees are inherently problematic. The red flag is when a contract uses fee language to create a termination penalty — a large lump sum that becomes payable if the seller cancels the engagement or the business fails to sell, regardless of whether a buyer was sourced or a transaction completed.

Red flags: Clauses that require the seller to pay a significant fee simply for withdrawing the business from the market or ending the engagement. These provisions sever the link between compensation and performance, weaken the broker's incentive to execute effectively, and shift execution risk almost entirely onto the seller. A broker who is paid for non-completion is no longer economically aligned with the outcome the seller actually cares about: a successful closing.

Example: If a broker values a small, owner-operated business at $600,000 and requires a $50,000 "minimum fee" that becomes payable if the seller terminates the engagement or the business fails to sell, that is not a retainer or a cost-recovery mechanism. It is effectively a guaranteed ~8% commission, regardless of outcome. By contrast, a modest retainer that covers actual preparation costs — or a minimum commission floor that applies only at closing — is far more consistent with market practice.

2. Success Fee Triggers

A success fee should incentivize and reward the broker for exactly that — success. A broker should earn a commission only when they successfully sell the business.

That's it.

What's market: For Main Street businesses, an 8–15% success fee earned only if a transaction closes, with the fee payable at closing from the proceeds of the sale. The IBBA reports that success-fees are the dominant form of compensation for businesses under $5 million in value.

Red flags: Success fees triggered without a closing. A success fee should be earned for one thing only: successfully closing a transaction. Any clause that allows a broker to earn a commission when no sale occurs breaks this core incentive structure.

Several contract provisions attempt to do this in different ways:

- "Ready, Willing, and Able" clauses — More common in real estate, these provisions state that the broker earns a fee if they introduce a buyer who claims to be "ready, willing, and able" to purchase at the asking price — even if the seller ultimately decides not to proceed or no transaction closes.

- Withdrawal-based triggers — Clauses that require the seller to pay the success fee if they withdraw the business from the market due to illness, personal circumstances, or changing market conditions.

- Financing failure triggers — Provisions that make the seller responsible for the broker's fee even when a deal collapses because the buyer fails to secure financing or satisfy other conditions.

- "Fulfilled obligations" language — Vague clauses stating that the broker earns the success fee once they have "performed their obligations" (such as marketing the business), regardless of whether a buyer closes.

While these provisions differ in form, they share the same effect: the broker gets paid without delivering the outcome the seller cares about. When compensation is no longer tied to a completed sale, the broker's incentives are no longer aligned with the seller's objectives.

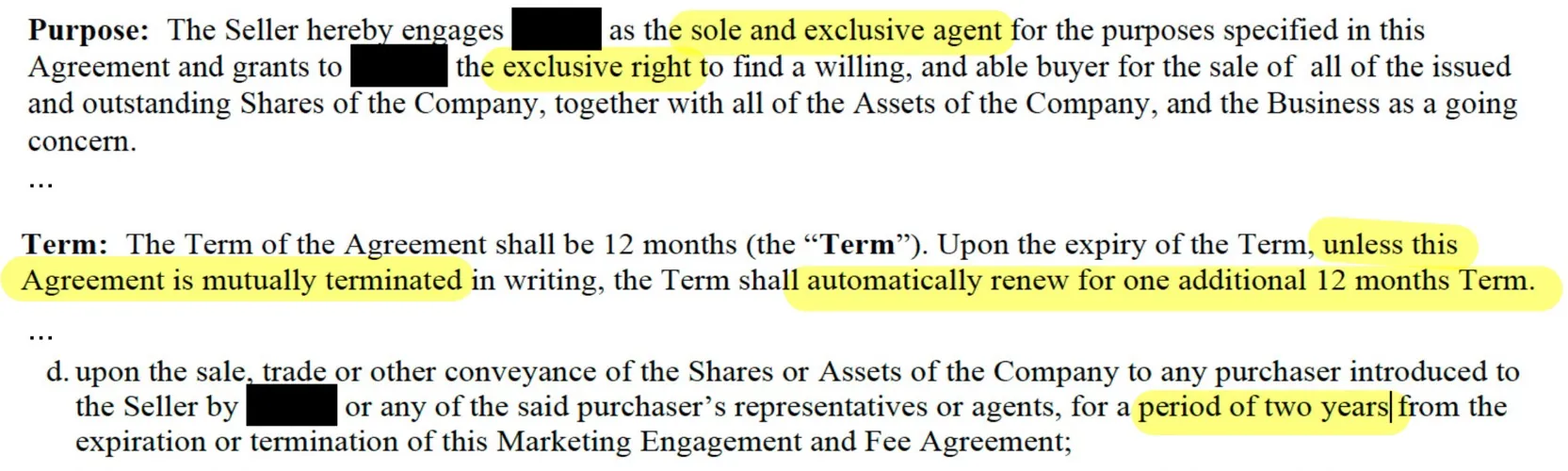

3. Tail Periods

A "tail period" is a window of time after the brokerage contract expires during which the broker is still owed a commission if the business sells.

Its legitimate purpose is to stop sellers from circumventing the broker — i.e., meeting a buyer introduced by the broker, waiting for the contract to expire, and then closing the deal privately to avoid paying the commission.

What's market: A 12-month period that applies only to buyers the broker can document they introduced, sent a CIM to, or actively negotiated with. The broker should provide a specific list of these names within 10 days of contract termination.

Red flags:

- Tails longer than 12 months.

- Universal tails: Clauses that apply to any buyer who purchases the business after the contract ends, even if the broker never met them.

- Broad definitions: Defining "introduced" to include anyone "associated with" a prospective buyer.

Real example of red flag language:

4. Exclusivity and Automatic Renewal

Broker exclusivity is standard. Brokers invest significant time and money upfront (marketing, valuation, vetting buyers) with no guarantee of pay. Without exclusivity, a seller could let three brokers do the work and only pay the one who crosses the finish line first, which disincentivizes quality representation.

However, while exclusivity is fair, indefinite exclusivity is not.

What's market: An exclusive period of 6 to 12 months. When that period ends, the contract should expire or require a mutual written agreement to renew. The typical small business sale takes 6 to 12 months, so a single exclusivity term should be sufficient for a well-executed engagement.

Red flags — Evergreen clauses (automatic renewal): Clauses stating the contract automatically renews for another 6–12 months unless the broker and seller mutually agree to terminate, or the seller cancels within a strict, small window (e.g., "between 30 and 45 days prior to expiration").

These clauses unnecessarily remove the seller's ability to reassess performance at the end of the exclusivity period and to decide — based on results — whether continuing the relationship makes sense.

Real example of red flag language:

5. Dual Agency

Dual agency means the broker represents both the buyer and the seller in the same transaction.

In residential real estate, dual agency is relatively common because the broker's role is largely transactional and standardized. In business sales, however, brokers are deeply involved in advising on valuation, deal structure, timing, and risk allocation. These elements directly affect price and outcomes for both sides.

A broker cannot simultaneously advise a seller on maximizing value and negotiating leverage while also advising a buyer on minimizing risk and purchase price. The conflict is structural, not theoretical.

In our opinion, reputable business brokers should not undertake dual agency mandates.

What's market: The broker represents the seller. The buyer signs a disclosure acknowledging the broker represents the seller's interests, and the buyer is encouraged to get their own representation.

Red flags:

- Pre-authorization: Clauses that pre-authorize dual agency and waive conflicts of interest before a buyer is even identified.

- Vague duty of care: Contracts that do not specify how the broker handles confidential pricing strategy if they end up representing the other side.

Real example of red flag language:

Quick Reference: Market Standard vs. Red Flag

| Clause | Market Standard | Red Flag |

|---|---|---|

| Retainers & minimum fees | Modest retainer credited against success fee; minimum commission floor payable only at closing | Large termination penalty payable on cancellation or if business fails to sell |

| Success fee | 8–15% of sale price, earned only when transaction closes | Fee triggered by "ready, willing, and able" buyer, seller withdrawal, financing failure, or "fulfilled obligations" |

| Tail period | 12 months, applies only to documented, named buyers | Longer than 12 months; applies to any buyer; broad definition of "introduced" |

| Exclusivity | 6–12 months, expires at end of term | Automatic renewal; narrow cancellation window; evergreen clauses |

| Dual agency | Broker represents seller only; buyer gets own representation | Pre-authorized dual agency; blanket conflict-of-interest waivers |

A Market-Standard Contract Checklist

Before signing a brokerage agreement, ask one simple question for every clause:

Does this clause exist to protect legitimate work — or to protect the broker from accountability?

1. Retainers and minimum fees are reasonable; no termination penalties

- ☐ Any upfront retainer is modest, reflects actual preparation costs, and is credited against the success fee at closing.

- ☐ Any minimum commission floor is proportionate to the deal size and payable only upon a successful closing.

- ☐ Cancelling the engagement or withdrawing the business does not trigger a large lump-sum payment or disguised commission.

2. Success fees are earned only upon a closing

- ☐ The broker earns a success fee only if a transaction actually closes and proceeds are received.

- ☐ There are no "ready, willing, and able," withdrawal-based, financing-failure, or "fulfilled obligations" clauses that trigger payment without a completed sale.

3. Tail periods are narrow, documented, and time-limited

- ☐ Any tail period is limited (typically no more than 12 months).

- ☐ Post-termination fees apply only to specific buyers the broker can document they introduced or actively engaged.

- ☐ The broker provides a clear, written list of tail buyers upon termination.

4. Exclusivity preserves seller optionality

- ☐ The exclusivity period is finite (typically 6–12 months).

- ☐ The agreement expires at the end of the term unless both parties affirmatively agree to renew.

- ☐ There is no automatic or "evergreen" renewal that limits the seller's ability to reassess performance.

5. Representation is clear and conflicts are not pre-waived

- ☐ The broker represents the seller only.

- ☐ There is no pre-authorization of dual agency or blanket waiver of conflicts before a buyer is identified.

- ☐ The contract clearly addresses how confidential information and negotiation strategy are handled.

If you are unsure whether a clause is market or not, get a second opinion before signing. Once signed, your leverage disappears.

Frequently Asked Questions

What should I look for in a business broker contract?

The five key areas to review are retainers and minimum fees (and whether they include termination penalties), success fee triggers, tail periods, exclusivity and automatic renewal clauses, and dual agency provisions. Retainers and minimum fees are standard and legitimate — the red flag is when fee language disguises a termination penalty that pays the broker even if no deal closes. For each clause, ask whether it aligns the broker's compensation with a successful closing — or whether it allows the broker to earn a fee without delivering a result. Use the checklist above as a starting point before signing any agreement.

How much does a business broker charge?

For Main Street businesses (typically under $5 million in value), the standard commission is a success fee of 8–15% of the sale price, paid by the seller at closing. Some brokers also charge a modest upfront retainer to cover preparation costs, which is often credited against the final commission. According to the IBBA Market Pulse Survey, success-fees are the dominant form of broker compensation in small business transactions. The specific percentage depends on the size and complexity of the deal — smaller deals typically command higher percentage commissions because the fixed costs of marketing and managing a sale are similar regardless of deal size.

What is a tail period in a business broker agreement?

A tail period is a window of time (typically 12 months) after a brokerage contract expires during which the broker is still owed a commission if the business sells to a buyer the broker introduced. Its legitimate purpose is to prevent sellers from meeting a broker-introduced buyer and then closing the deal privately after the contract ends. A fair tail clause should apply only to specifically named buyers and require the broker to provide a documented list upon termination.

What is dual agency in a business sale?

Dual agency occurs when the same broker represents both the buyer and the seller in a transaction. While common in residential real estate, dual agency in business sales creates a structural conflict of interest: the broker cannot simultaneously advise the seller to maximize price while advising the buyer to minimize it. Reputable business brokers typically represent the seller only, with the buyer encouraged to retain their own representation. Watch for contract clauses that pre-authorize dual agency before any buyer has been identified.